Every two years, the Wisconsin Worker’s Compensation Advisory Council (WCAC) negotiates a bill that goes off to the legislature for consideration. The WCAC, made up of 5 representatives from management and 5 representatives from labor, tries to come to agreement on a bill that makes modifications to the Worker’s Compensation Act. It has a long standing history in our State, with each side attempting to get changes that benefit those they represent.

Every two years, the Wisconsin Worker’s Compensation Advisory Council (WCAC) negotiates a bill that goes off to the legislature for consideration. The WCAC, made up of 5 representatives from management and 5 representatives from labor, tries to come to agreement on a bill that makes modifications to the Worker’s Compensation Act. It has a long standing history in our State, with each side attempting to get changes that benefit those they represent.

There are several potential changes that are noteworthy for this cycle. Here is a summary of the big items:

- Fee Schedule: Both sides have agreed that there is a need for a fee schedule as a way to better control medical expenses. We are one of the few States in the country that has no fee schedule. As a result, it’s not uncommon for a work related medical procedure to cost two to three times more than the same procedure that is non-work related. The challenge here is that the fee schedule has not yet been developed and it is supposed to be based on negotiated health insurance rates. Networks are very protective of the rates that they have negotiated with providers. I see that as an obstacle. The other component of this proposal is that any savings realized from the fee schedule are to be shared with injured workers. Call me a pessimist, but I will be surprised if this ends up looking anything like what the management representatives envisioned.

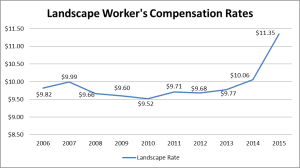

- Permanent Partial Disability: Permanent Partial Disability rates will increase substantially over the next two years. The current rate is $362. That will increase to $382 in 2018 and $407 in 2019. Those are some hefty benefit increases at 5.5% and 6.5% respectively. How do those percentage increases compare to your budget for merit increases?

- Injury Multiplier: This provision could prove to be quite expensive for businesses. This will allow an additional 15% in benefits to workers with scheduled injuries who are not able to come back to work within 85% of their pre-injury wage. This is a benefit that did not exist in the past.

It appears as though the management representatives gave some big increases in indemnity benefits in hopes that savings from a fee schedule will offset those increases. Time will tell.

There are several other proposals as part of this agreed bill that will impact the premiums moving forward including supplemental benefits, loss of hearing and treatment of opioids. For a full list of changes, click here.

Please feel free to reach out to me if you would like to better understand how these changes could impact your worker’s compensation premiums.

It’s not something that most people think about, but just like your business, NFL teams also have to purchase worker’s compensation insurance for their employees. And just like the benefits that are afforded your employees, football players are covered for lost wages, medical treatment, loss of earnings, etc.

It’s not something that most people think about, but just like your business, NFL teams also have to purchase worker’s compensation insurance for their employees. And just like the benefits that are afforded your employees, football players are covered for lost wages, medical treatment, loss of earnings, etc.  ith another year in the books, we took a look back at the top 5 most popular R&R articles of last year.

ith another year in the books, we took a look back at the top 5 most popular R&R articles of last year. The Wisconsin Compensation Rating Bureau is now requiring a mandatory audit noncompliance charge (ANC). Effective January 1, 2017 any insured who does not comply with a workers compensation audit will be billed an additional two times the estimated workers compensation premium.

The Wisconsin Compensation Rating Bureau is now requiring a mandatory audit noncompliance charge (ANC). Effective January 1, 2017 any insured who does not comply with a workers compensation audit will be billed an additional two times the estimated workers compensation premium. In July 2016, the new Work Comp rates for policies, effective October 1st, 2016, were released. Generally speaking, the rates went down by an average of 3.19%, which is great news.

In July 2016, the new Work Comp rates for policies, effective October 1st, 2016, were released. Generally speaking, the rates went down by an average of 3.19%, which is great news. Wearable devices are becoming increasingly common in the workplace. While certain organizations have been using these tracking devices to promote healthy habits among their employers, the discussion surrounding identifying potential injuries and reducing the frequency of workers comp claims is growing.

Wearable devices are becoming increasingly common in the workplace. While certain organizations have been using these tracking devices to promote healthy habits among their employers, the discussion surrounding identifying potential injuries and reducing the frequency of workers comp claims is growing. Henry Ford once said “chop your own wood and it will warm you twice.” I’m here to tell you now’s the time to evaluate your pre-loss and post loss workers compensation strategies and it will warm you even more.

Henry Ford once said “chop your own wood and it will warm you twice.” I’m here to tell you now’s the time to evaluate your pre-loss and post loss workers compensation strategies and it will warm you even more.