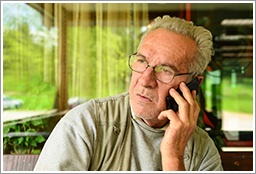

It starts off just like any other telemarketer phone call: "We are sending out new Medicare cards and have just a couple simple questions for you. Can you confirm you name, address, and phone number."

It starts off just like any other telemarketer phone call: "We are sending out new Medicare cards and have just a couple simple questions for you. Can you confirm you name, address, and phone number."

You easily reply "yes, that is correct."

The telemarketer starts listing off numbers and asks "please confirm that is your bank routing number."

RED FLAG!

Health insurance scams are increasing every day across the country. Many are preying on the mass confusion over the health care system. And unfortunately Senior Citizens are often the targets: they are home more often to answer the phone and generally have larger retirement savings for scammers access.

Due to the confusion with healthcare, other scams include offering fake health coverage, bare-bones policies being sold as full coverage, and fake Obamacare coverage.

Tips to help avoid falling victim to a scam:

- Don't answer the phone too quickly - check caller ID if possible

- Think about the question they are asking

- Think before you answer the question

- NEVER give out personal or financial information over the phone

- Just hang up the phone

Wisconsin residents with questions on how health care reform will affect you, please contact knowledgebroker Pete Frittitta.