Large Rate Increase for Landscapers Effective 10/1/15

Over the past 9 years or so, worker’s compensation rates for Wisconsin landscapers have remained relatively flat. Business owners have benefited from predictability in costs for their most expensive line of casualty insurance. With the new rates effective for 10/1/15 – 9/30/16, owners should be prepared for an invasion on their bottom line similar to the effect the Emerald ash borer has had on unprotected ash trees.

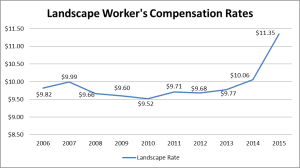

With rates averaging about $9.72 for every $100 of landscape payroll from 2006 – 2013, the industry saw a 3% rate increase in 2014. This year, with a new rate of $11.35, you are facing a 12.8% increase compared to last year.

Unfortunately, you have no control over the landscape rate that is calculated by the Wisconsin Compensation Rating Bureau. You do, however, have control over many other aspects of your business that will have a direct impact on what you pay for your worker’s compensation insurance. But like every great landscaping project, it requires a vision and a plan. Do you have a plan in place to prepare yourself for substantial worker’s comp premium increases next year?